Rear-end collisions are the most common type of accident on Georgia roads. Most drivers assume that because the damage looks contained to the bumper and trunk area, the financial hit ends when the repair bill is paid. That assumption is wrong, and it costs Georgia drivers real money every year. A rear-end collision leaves a permanent mark on your vehicle’s history that buyers can see, insurers use to discount value, and the market prices in immediately. That loss has a name: diminished value. And in Georgia, you have the legal right to recover it from the at-fault driver’s insurance company.

Why Rear-End Collisions Hit Modern Cars Harder Than You Think

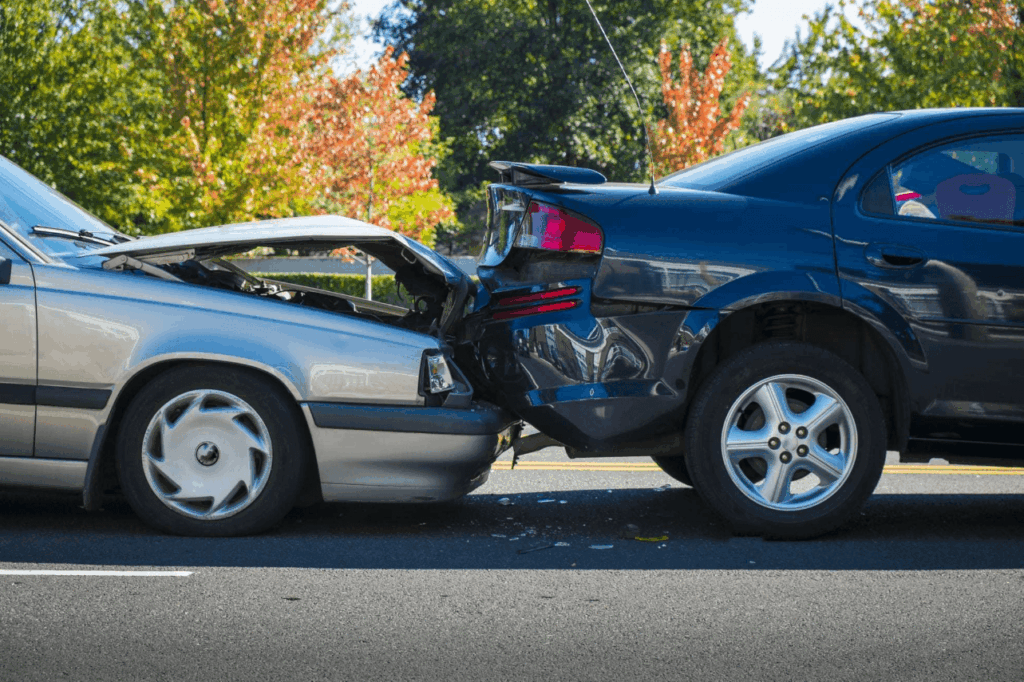

A decade ago, a rear-end collision was often a straightforward bumper repair. Today it is a completely different situation. Modern vehicles pack the rear end with technology that did not exist in previous generations: backup cameras, parking sensors, radar-based blind spot monitors, cross-traffic alert systems, and in many cases, components tied directly to the adaptive cruise control system. Every one of those elements sits in or near the rear bumper fascia.

When that zone takes an impact, the visible damage is only part of the story. Sensors get knocked out of calibration. Radar modules get displaced. Cameras crack or shift. The structural foam behind the bumper cover compresses in ways the factory never intended. Even a low-speed hit at 15 mph can trigger a repair estimate with three or four line items for ADAS recalibration alone, on top of the body work.

This matters for your diminished value claim because the nature and complexity of the repair directly affects how the market perceives your vehicle after the fact. A Carfax showing rear-end structural damage and ADAS-related repairs signals more risk to a future buyer than a simple fender replacement. That perception translates into a lower offer at resale, and that lower offer is the financial loss you are entitled to recover.

Key point: Diminished value is not calculated from the repair cost. It is calculated from the gap between what your vehicle was worth before the accident and what it is worth after, based on real market conditions. Rear-end collisions with ADAS involvement consistently produce larger gaps than surface damage alone suggests.

The Carfax Problem: What Buyers Actually See

When you sell a vehicle in Georgia, the first thing any serious buyer does is pull the vehicle history report. Carfax and AutoCheck both flag accident involvement. What shows up on that report is not a nuanced description of a minor fender bender. It is a data point that reads as a structural or collision event, and buyers respond to that data by negotiating the price down or walking away.

Studies on vehicle history stigma consistently show that accident-flagged vehicles sell for less than clean-history equivalents, even when the repairs were done perfectly and there is no mechanical issue to speak of. The market does not care how well your body shop did the work. It cares that the accident happened.

For rear-end collisions specifically, the stigma is compounded when the repair record includes structural components. Frame straightening, rear rail repair, or any notation of unibody work will show up in an appraiser’s review of the repair order and in how comparable sales are adjusted. Vehicles with that kind of documented history trade at a steeper discount than those with cosmetic-only damage, even within the same make, model, and year.

How Georgia Law Applies to Your Rear-End Collision Claim

Georgia is one of the clearest states in the country when it comes to third-party diminished value rights. The Georgia Supreme Court ruling in State Farm Mutual Automobile Insurance Co. v. Mabry established that the at-fault driver’s insurer is obligated to compensate you for your vehicle’s full property damage, including the permanent loss in market value caused by the accident history. That ruling did not carve out exceptions for rear-end collisions, minor damage thresholds, or vehicle age. If the accident was not your fault and your vehicle lost value, you have a claim.

There is one practical requirement: the accident needs to be on record as the other driver’s fault. In rear-end collisions, fault is typically clear. The driver who struck your vehicle from behind is almost universally assigned liability under Georgia traffic law. That makes rear-end collisions one of the cleanest situations to file a diminished value claim from a legal standing perspective.

The Georgia statute of limitations for property damage claims gives you four years from the date of the accident. That window is longer than most drivers realize, but waiting weakens your case. Repair documentation gets harder to obtain, comparable sales data drifts, and the connection between the accident and your vehicle’s current market position becomes more difficult to establish clearly. The full breakdown of how long you have to file a diminished value claim in Georgia explains exactly why timing matters beyond just the legal deadline.

What Factors Drive the Diminished Value Amount After a Rear-End Hit

Not every rear-end collision produces the same diminished value. The amount depends on several factors that interact with each other, and understanding them helps you set realistic expectations before you engage with the insurer.

| Factor | Lower DV Impact | Higher DV Impact |

|---|---|---|

| Vehicle age | Older, higher mileage | Newer, lower mileage |

| Repair scope | Cosmetic only, no structural | Frame, rails, ADAS components |

| Vehicle segment | High-volume economy sedan | Luxury, truck, SUV, EV |

| Pre-accident condition | Prior accident history on file | Clean title, no prior accidents |

| Market demand | Low-demand model in Georgia | High-demand model, limited supply |

A 2023 pickup truck with 18,000 miles that took a rear-end hit requiring frame rail repair and ADAS recalibration is going to produce a significantly different claim than a 2018 sedan with 90,000 miles that needed a bumper cover and tail light. Both vehicles lost value. The question is how much, and the only way to establish that number with any credibility is through an independent professional appraisal.

Why the Insurer’s First Offer Is Almost Never Accurate

When you file a diminished value claim after a rear-end collision in Georgia, the at-fault driver’s insurer will eventually respond with a number. That number is rarely based on your vehicle’s actual market loss. It is almost always based on the 17c formula, an internal insurance industry tool that applies a fixed percentage cap of 10% of your vehicle’s pre-accident value, then applies a series of multipliers that reduce the figure further based on damage severity and mileage.

The problem is structural. The 17c formula was never designed to calculate actual market loss. It was designed as an internal budgeting tool. Applying it to a modern vehicle with ADAS components, strong market demand, and a clean title history before the accident produces results that bear little resemblance to what comparable vehicles actually sell for in the Georgia market. Independent appraisals based on real comparable sales consistently show larger losses than the 17c formula produces.

This is not a small discrepancy. On a vehicle worth $38,000 before the accident, the gap between a 17c-formula offer and an independent appraisal result can easily run into thousands of dollars. The question is whether you have the documentation to push back.

Accepting the insurer’s first diminished value offer without an independent appraisal is the single most common mistake Georgia drivers make after a rear-end collision. Once you accept, the claim is closed.

What to Do After a Rear-End Collision in Georgia to Protect Your Claim

The steps you take in the days and weeks after a rear-end collision directly affect how strong your diminished value claim will be. Most of this is simple documentation discipline.

- Get the police report. Even if the damage looks minor at the scene, an official accident report locks in the fault determination. Request a copy as soon as it is available.

- Photograph everything before repairs start. Take photos from multiple angles, including under the bumper, inside the trunk, and any visible sensor or camera components. Your body shop may not document pre-repair condition in the detail you need.

- Request the full repair order. Ask the shop for a line-by-line repair order showing exactly what was replaced, repaired, and recalibrated. This document is foundational to your appraisal. Our guide on what documents you need for a diminished value claim in Georgia walks through each item in detail.

- Do not accept the repair-only settlement as your final resolution. The repair payment and the diminished value claim are two separate transactions. Accepting payment for repairs does not close your DV claim.

- Get an independent appraisal before engaging with the adjuster on DV. This gives you a defensible number to negotiate from rather than responding to whatever the insurer offers first.

EVs and Rear-End Collisions: A Higher-Stakes Situation

Electric vehicles deserve a separate mention here because the stakes are substantially higher. In many EV architectures, the battery pack runs close to the rear of the vehicle. A rear-end collision that appears to involve only the bumper zone may have caused proximity damage to the battery enclosure or associated high-voltage components. Repair facilities with genuine EV certification are rare, and insurers are still working out how to value EV-specific damage consistently.

What that means in practice is that a rear-end collision on an EV can produce both a larger repair scope and a larger market stigma than the equivalent collision on a traditional internal combustion vehicle. Buyers of used EVs are particularly sensitive to accident history in the rear zone precisely because of battery proximity concerns. That translates directly into a larger diminished value loss that deserves to be documented and recovered accordingly.

What a Professional Appraisal Actually Looks Like

A credible diminished value appraisal for a rear-end collision in Georgia is not a generic estimate generated by a formula. It starts with the repair documentation, assesses the nature and severity of the damage, identifies the vehicle’s pre-accident market value using current comparable sales in the Georgia market, and then calculates the specific market value reduction caused by the accident history being permanently attached to that VIN.

The appraiser’s report needs to be detailed enough to withstand scrutiny from the insurer’s adjuster and, if the claim escalates, from a Magistrate Court proceeding. That means specific comparable sales data, clear methodology, and a final number that can be explained and defended. Cookie-cutter reports based on database lookups do not hold up. What actually gets claims paid is documented market evidence. Understanding how to prove a diminished value claim in Georgia is the foundation for getting a fair settlement.

If you are not sure whether your rear-end collision qualifies or what the potential recovery might look like, a free estimate is the logical first step before committing to anything.

Your Rear-End Collision May Be Worth More Than the Repair Bill

Georgia law gives you the right to recover the market value your vehicle lost after an accident. Get a free estimate from Georgia’s most experienced DV appraisers and find out exactly what your claim is worth. Get Your Free DV Estimate

Download This Article as a PDF

Save or share the full guide on rear-end collision diminished value claims in Georgia.

Frequently Asked Questions

Can I file a diminished value claim if the rear-end collision was minor and my car looks fine after repairs?

Yes. The key factor is whether the accident shows up in your vehicle’s history report and whether that history affects what buyers are willing to pay. Even cosmetic rear-end repairs leave a permanent Carfax record. For newer vehicles with low mileage, even minor accidents produce documentable market value losses. Whether the claim is worth pursuing depends on your specific vehicle and the repair scope, which is why a free estimate is the right starting point.

The at-fault driver’s insurer already paid for my repairs. Does that close my diminished value claim too?

No. The repair payment and the diminished value claim are legally separate. Accepting payment for physical repairs does not settle or waive your right to file a separate claim for the loss in market value. You should review any release language before signing anything from the insurer to make sure you are not inadvertently closing your DV claim as part of the repair settlement.

How does ADAS recalibration after a rear-end collision affect my diminished value?

ADAS involvement in a repair increases the perceived risk profile of the vehicle for future buyers and appraisers. Systems like radar-based collision avoidance, blind spot monitoring, and automated emergency braking need to be precisely calibrated to function correctly. Even with a successful recalibration, the repair record showing ADAS component work signals to buyers that the vehicle sustained an impact complex enough to require that level of intervention. That signals higher risk and lower resale offers.

What if the insurer denies my diminished value claim after a rear-end collision?

A denial is not the end of the process. Georgia law is clear that third-party diminished value claims are recoverable, and insurers cannot categorically deny them. Your next steps include sending a formal demand letter backed by your independent appraisal report, filing a complaint with the Georgia Office of Insurance and Safety Fire Commissioner, or taking the claim to Magistrate Court. The full process is covered in the guide on what to do when your diminished value claim is denied in Georgia.

Does the 17c formula apply to my rear-end collision diminished value claim?

Insurance companies use the 17c formula routinely because it produces low numbers and is difficult to dispute without independent data. It is not a legally required standard in Georgia, and courts have accepted independent appraisals based on comparable market sales as more accurate representations of actual loss. If the insurer uses the 17c formula to produce an offer, that offer is a starting position, not a final word. An independent appraisal gives you the evidence to challenge it.