TYPICAL APPRAISAL CLAUSE FOUND IN MOST GEORGIA POLICIES

TYPICAL APPRAISAL CLAUSE FOUND IN MOST GEORGIA POLICIES

This article only applies to claims filed against your own policy/carrier, irrespective of fault (first party claims).

To hire us to negotiate an appraisal clause with your carrier, please visit our claim management and settlement page.

Note: Some Safeco and Auto Owners insurance policies don’t have an appraisal clause. State Farm’s appraisal clause applies only on the vehicle’s actual cash value but they will hire an appraiser for DV once the claim is escalated. Infinity insurance policies contain an appraisal clause but the carrier to refuses to apply it on DV claims. Regardless of the existence of an appraisal clause, insurance carriers are required by law to handle claims in good faith which includes considering evidence submitted by an insured.

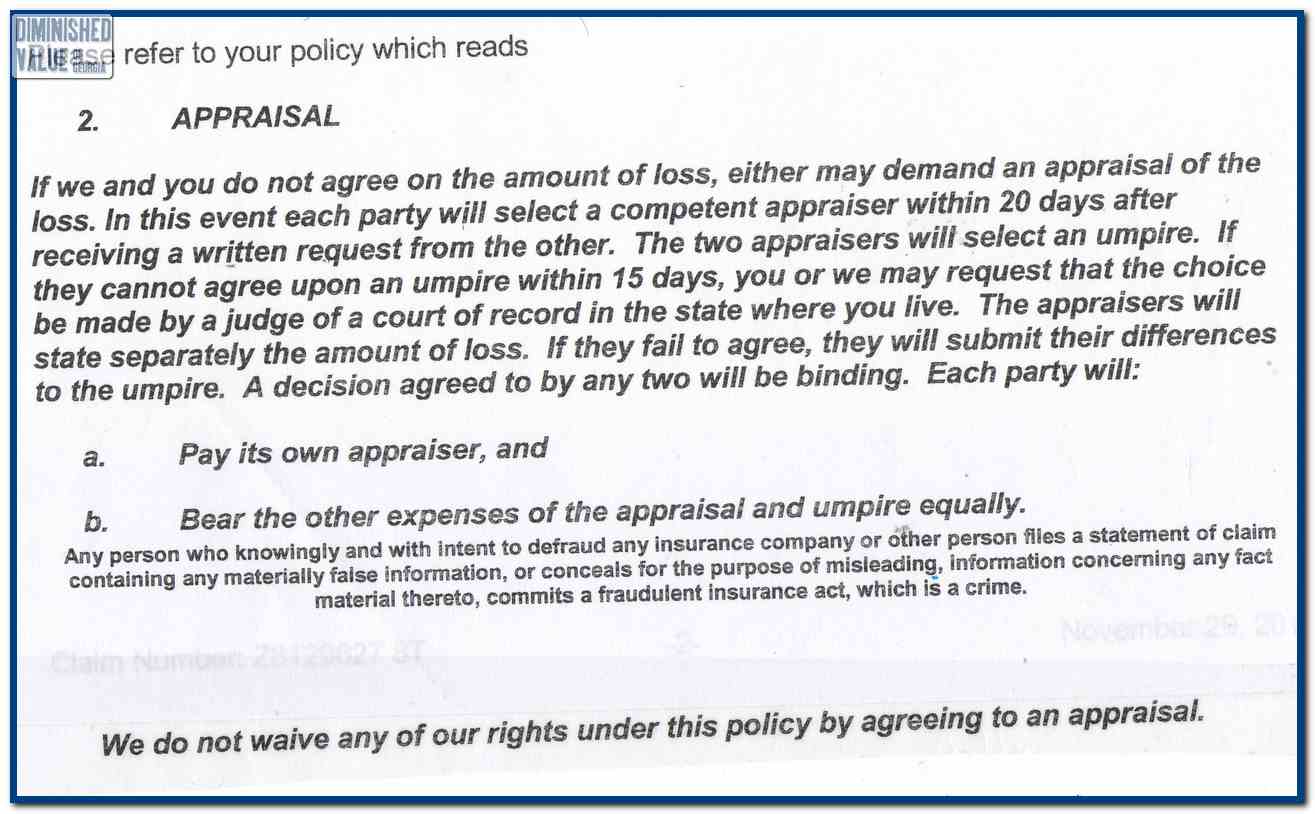

APPRAISAL

If you (insured, vehicle owner) and we (insurance company or insurer) fail to agree on the amount of loss (total loss or loss in value), either one can demand the loss to be set by appraisal. Either side shall make a written demand for appraisal, each side shall select a competent, independent appraiser. The appraisers shall then set the amount of loss. If the two appraisers fail to agree within a reasonable time, they shall submit their differences to the umpire. Written agreement by any two is binding. The cost of hiring the umpire shall be divided equally between the insurer and the insured.

Sample Auto Insurance Policy with appraisal clause

Another Insurance Company Appraisal Clause

Selection of an Appraiser

Appraisers are required to be independent. If either party appoints an Appraiser whose primary income is dependent upon the appointing party, or if the Appraiser is not competent, the entire process could be found flawed and the ruling overturned.

It’s important to understand that a good Appraiser is someone who understands insurance issues and in knowledgeable in the field. An Expert.

Regardless of background, the person appointed as Appraiser needs to be a skilled communicator and advocate. He or she should not be unreasonable during the process.

Some insurance companies will not hire an independent appraiser but will choose an “in-house” adjuster to fill the position. This adjuster is usually a salaried employee of the insurance company. This defeats the spirit of the appraisal clause and will render the process biased and unfair.

If your insurance company hires an in-house appraiser for an appraisal clause dispute, you need a new carrier.

If your policy does not have an appraisal clause or chooses not to apply the appraisal clause on diminished value claims, you need a new carrier.

Appointment of an Umpire

The Umpire is supposed to be an unbiased third appraiser. Usually the two main appraisers (the one representing the insured and the one representing the insurer), will try to settle the claim without the need for an umpire.

If the Appraisers reach an agreement, an Umpire is no longer required. Any agreement made (either by the two Appraisers or by the Umpire and one of the appraisers) must be in writing and furnished to all parties. The Umpire’s ruling only needs to be agreed to by one of the Appraisers.

Hiring a competent appraiser will eliminate the need for an umpire

In Georgia, there is small number of independent auto appraisers specializing in Diminished Value, due to the large number of claims processed, these appraisers interact with each other on a regular basis creating an amicable “settlement zone” where appraisers usually settle claims fairly and quickly without the need for an umpire.

This process is interrupted when the insured (you) hires an out of state appraiser or appraisal company that the local “insurance” appraiser is not familiar with or does not find credible. In this case the “insurance” appraiser will immediately opt for an umpire therefore increasing your out of pocket expense and rendering your appraisal moot. The appraiser representing the insurer is REQUIRED to inspect your vehicle, usually requiring your appraiser to do the same.

It is rare to find a qualified umpire that agrees with an “online” or unreliable out of state appraiser. Also, ordering an appraisal report online without an actual appraiser handling and negotiating the claim is useless. If the two appraiser cannot TALK, they cannot SETTLE !

What The Appraisal Process Can Do For You

The appraisal process can be an effective tool in expediting settlement of your claim. With the proper appraiser, claims can be quickly and effectively settled.

The Settlement Process

After receiving an unfavorable offer from your insurer, usually an offer based on 17c, you should contact us.

We will conduct a free claim review and will advise as to what the real loss in value (or total loss) amount should be. We will then inspect your vehicle and provide you with our appraisal report.

After you receive our appraisal report and in writing, using a cover letter we help you draft, you will inform your insurance adjuster of your intent to invoke your policy’s appraisal clause.

Many insurance companies, realizing they have an informed and educated consumer on their hands, will, in good faith, offer to settle the matter at the amount requested in your appraisal. Some insurance companies will try to counter-offer and some will hire their own appraiser.

Regardless of the insurance company’s decision, you have effectively shifted the settlement and compensation process away from the erroneous and low ball initial amount.

If the insurance company hires their own appraiser, they no longer have control over the settlement amount.

If your insurance company tries to counter offer, usually offering a percentage of your demanded amount, listen to what they have to offer but know that you can always demand to pursue the appraisal clause as written in your policy.

If the insurance company hires their own appraiser, no problem, at no additional cost to you, we will negotiate the loss amount with their appraiser and settle the claim at a mutually favorable sum. The appraisers cannot be influenced by the principals, the settlement amount is binding and the claim closed.

The settlement amount achieved by the two appraisers is final and can only be rescinded if the appraisal clause is off the table and the initial insurance company offer is accepted. This is never the case, the settlement amount is usually much higher than the original amount.

I hope this article was helpful, please call us at 678-404-0455 if you have more questions.

Want to hire to negotiate and settle a claim for you? Please fill out the form below. Thank you.

{kind=link}