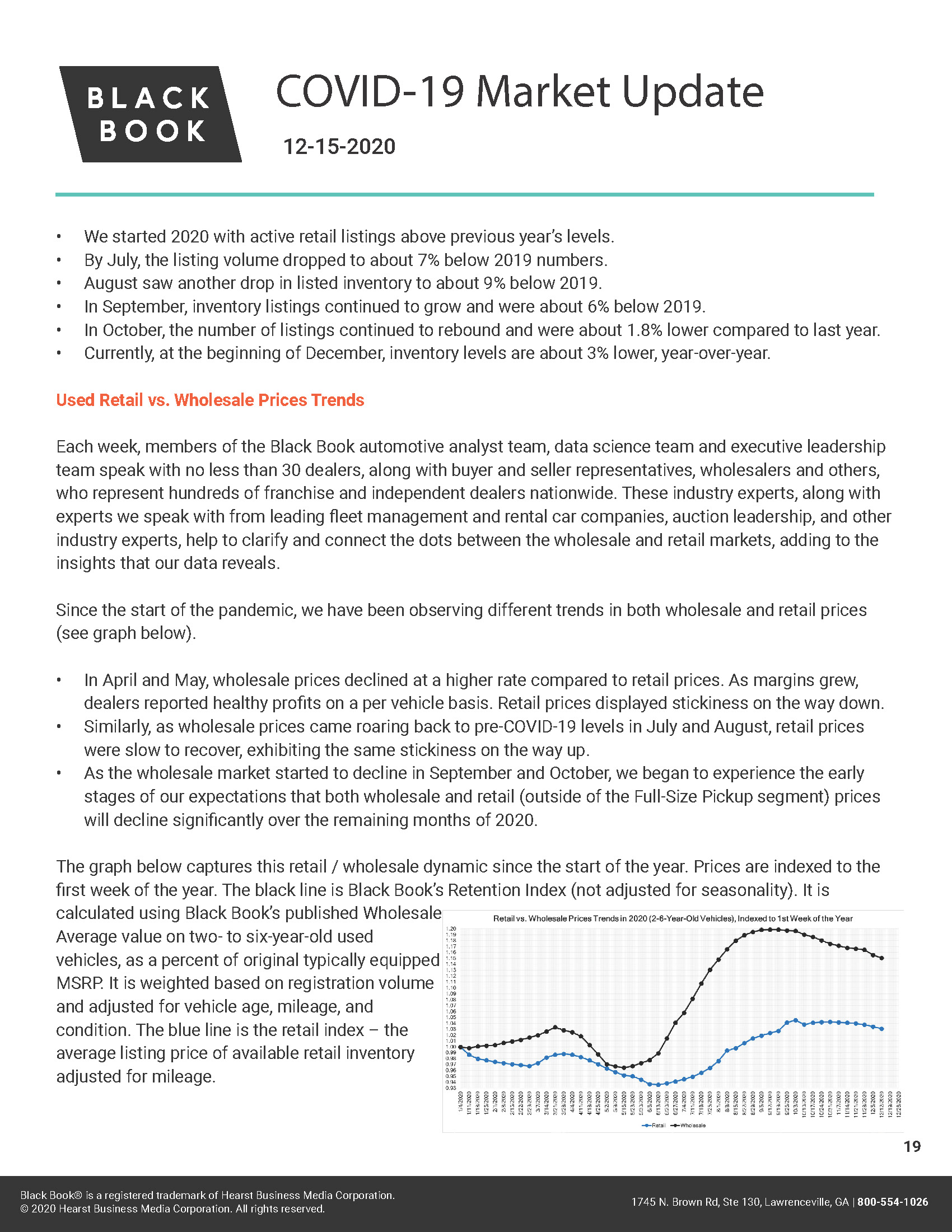

Recap of Auto industry-related headlines over the last week:

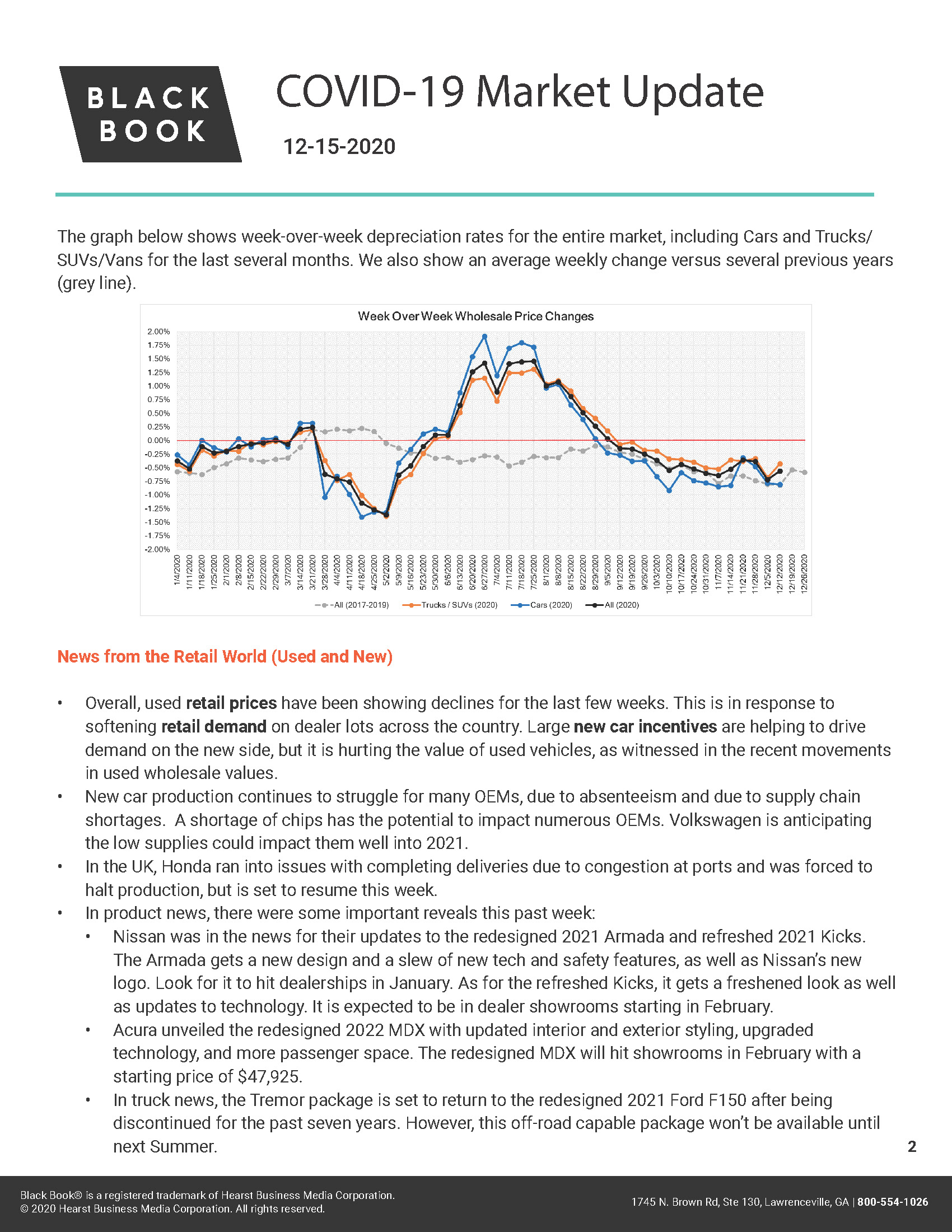

- Wholesale prices continued their decline last week, for the fourteenth week in a row.

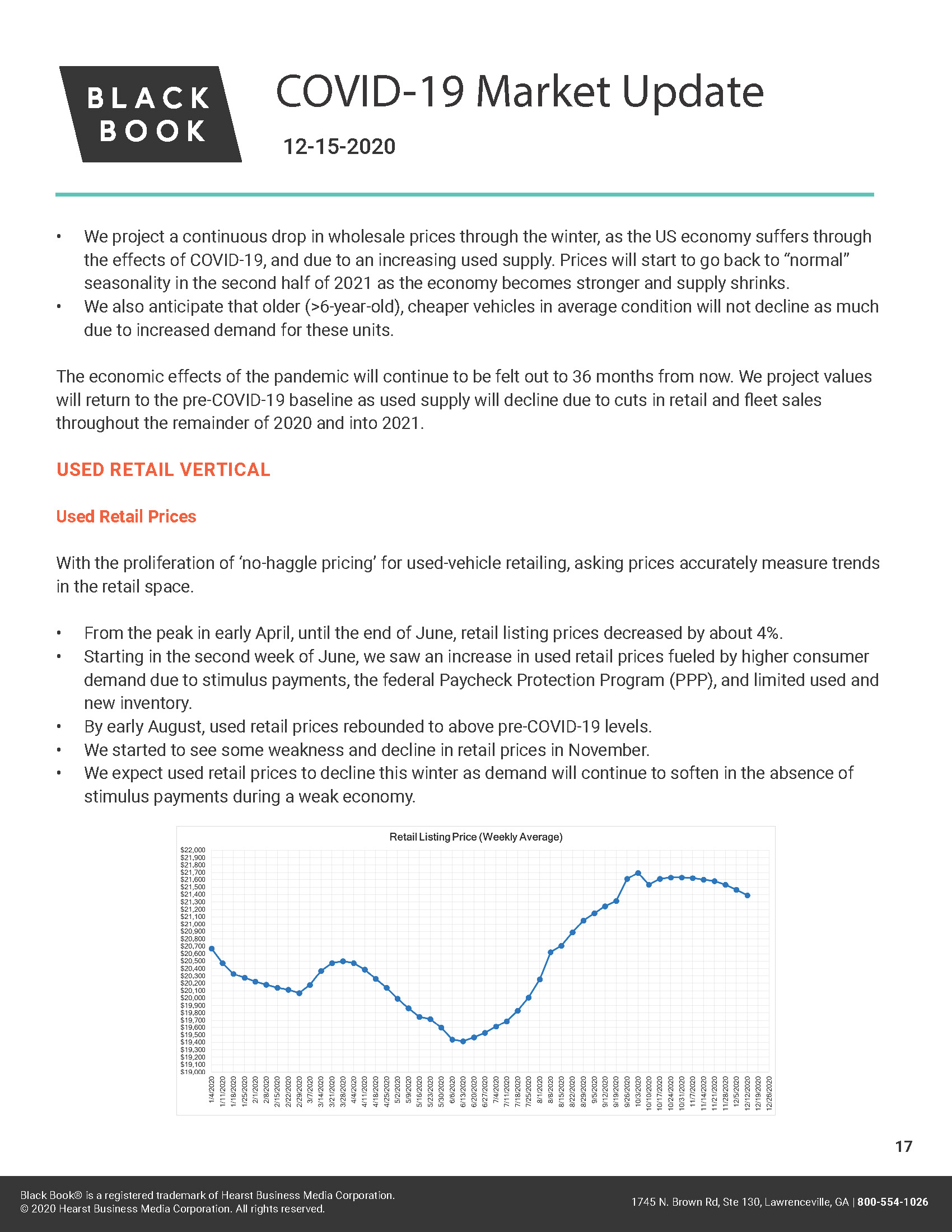

- Average retail listing prices of available inventory have been essentially flat over the last two months, but overall pricing began to show signs of softening over the last three weeks. Full-Size Truck retail prices have also started to show small signs of softening; however, values remain well above last year.

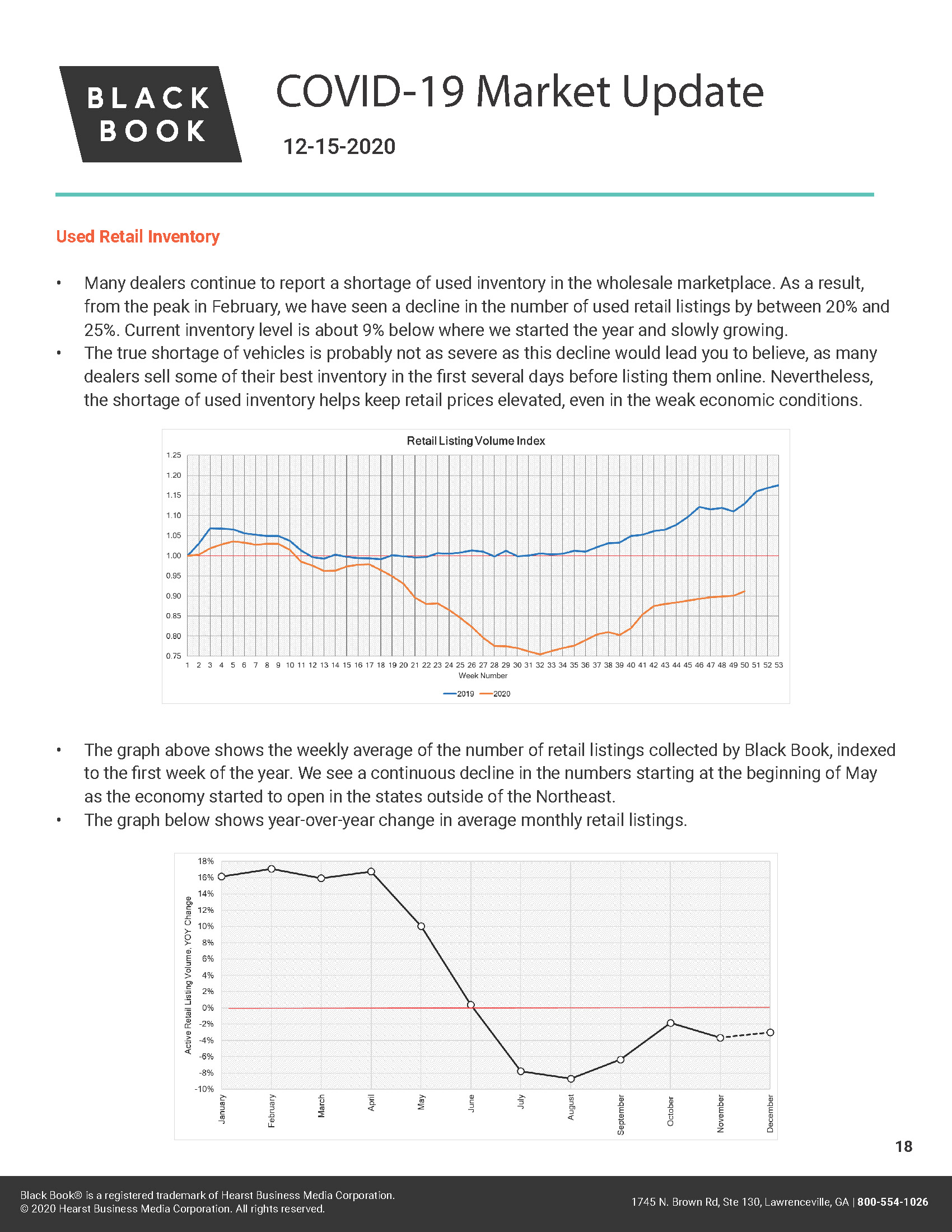

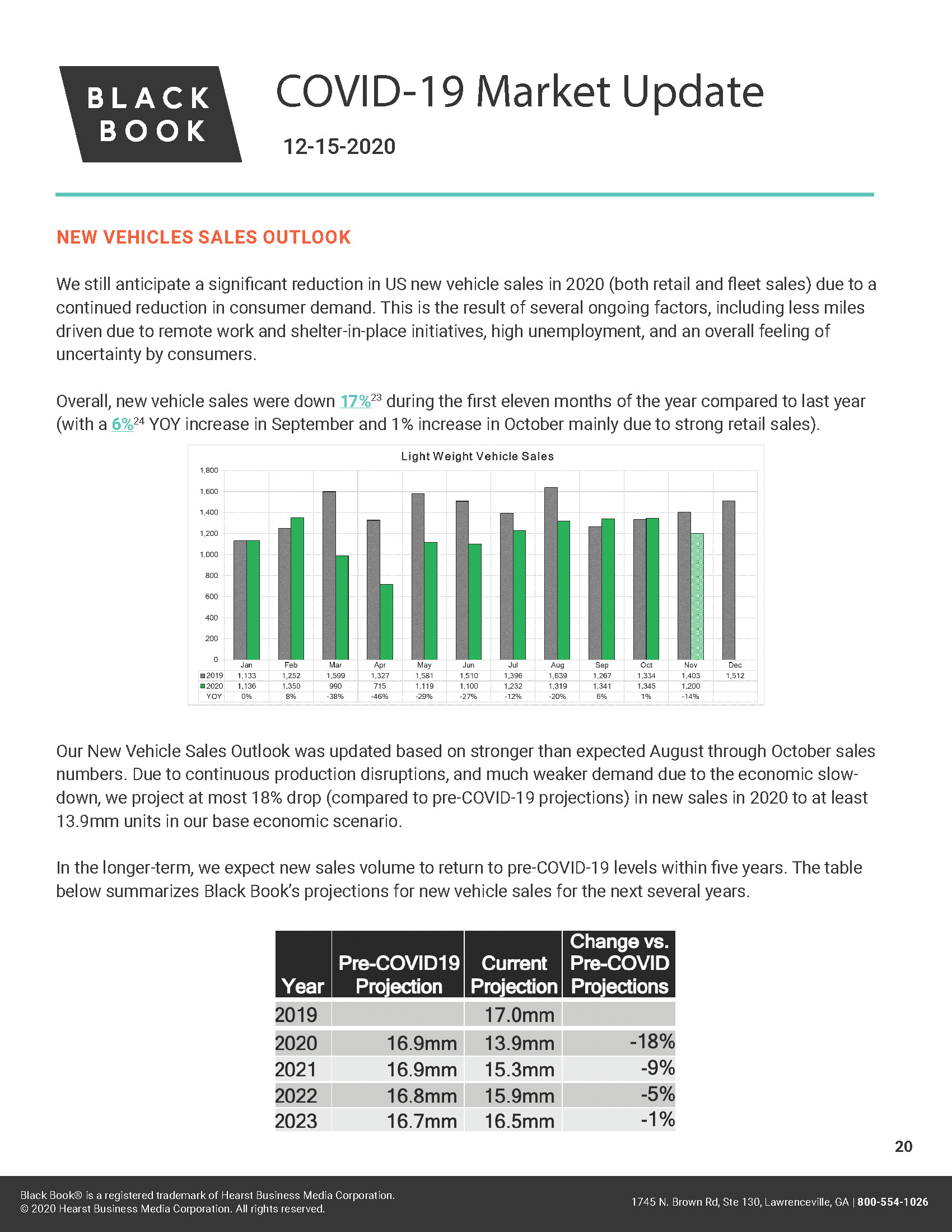

- Used retail listing volume continued to increase last week but remains at levels lower than last year – about 3.0% below the prior year, and 9% below where the industry began in 2020.

Current Wholesale Market Overview

- Remarketing strategies are widely varying right now with some remarketers finding themselves low on volume and holding firm to floors, while others are seeing volumes rise and are finding the need to aggressively sell off units. Overall sales rates this past week increased with many remarketers ready to strike deals with dealers. The auctions with buyers and sellers physically present are able to take advantage of the situation and have successful in-lane negotiating.

- High condition scores and low mileage units continue to garner the most attention on the lanes, but as new retail units are seeing increases in incentives levels, it is starting to show signs of softening the used market.

- Repossessions still aren’t showing up in any volume on the lanes, but we are starting to see “voluntary repossessions” available in small quantities. This is traditionally a slower time of year for repossessions so the expectation is that portion of the used market will pick up in 2021.

Automotive Market Update for December 2020 (pdf)